insurance between retirement and medicare - Approaching Medicare Options

insurance between retirement and medicare - Approaching Medicare Options

We get many calls these days to the tune of...

"What's the cheapest way to insure till Medicare starts?"

It's a good question.

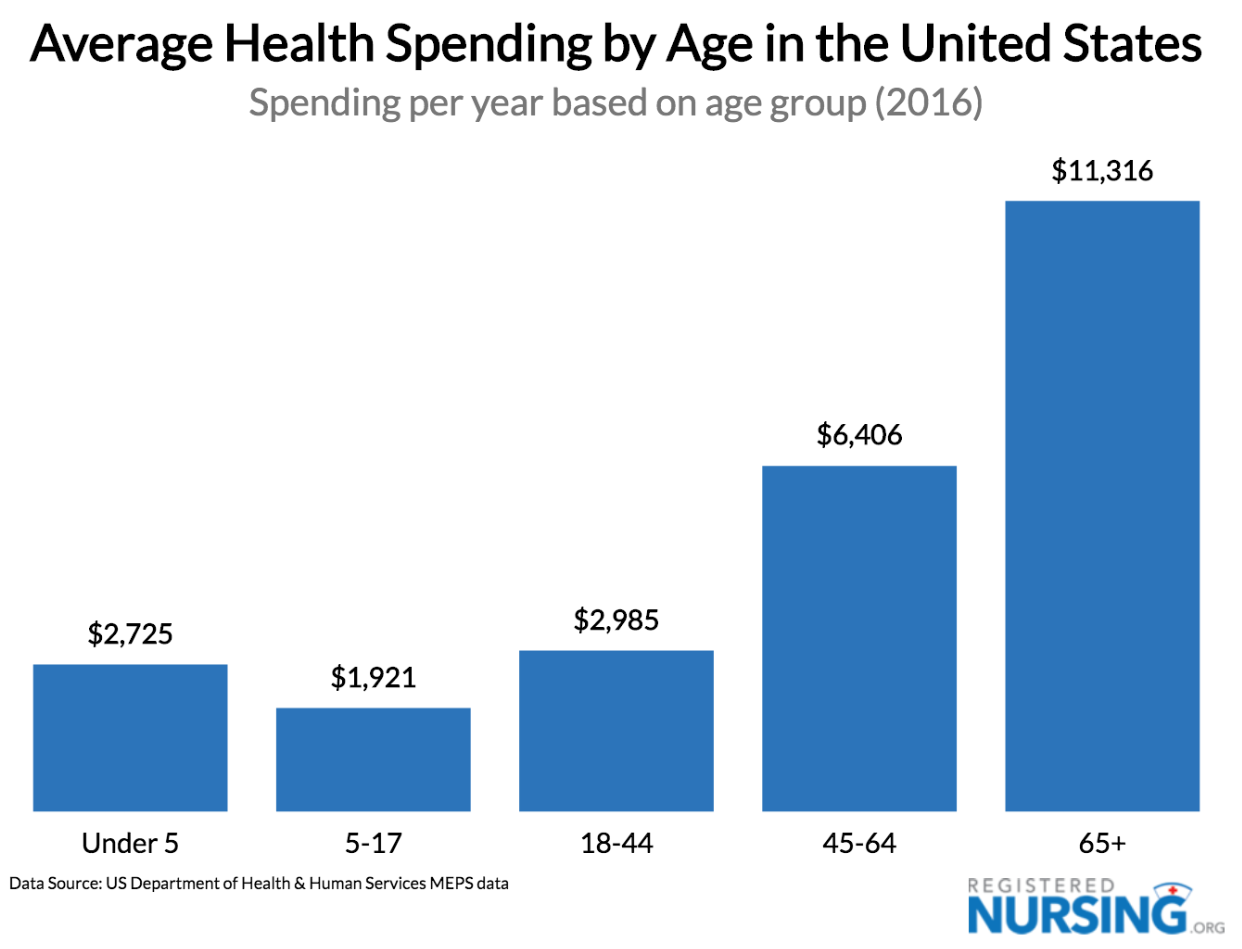

For one reason, health insurance is the most expensive when you're in your 60's.

Age 64 is literally the most expensive time to insure in a person's life!

- Medicare hasn't started yet for most people.

- Age 65 is the time Medicare starts for most people.

- Many people retire prior to the turning 65 and being eligible for Medicare.

Don't take our word for it...

How do we address this gap?

Great question.

Let's go through the three main options:

- Cobra coverage if available

- Covered California

- Short term health insurance

We're happy to walk through any questions you have.

We have wonderful tools for people entering Medicare...so you can manage the onslaught of flyers and brochures you're about to get!:

- How to pick the best Medicare plan

- The trade-off between Advantage plans and Supplements

- How and When to Enroll in Medicare

Don't take our word for it...

Finally, you can quote Medigap plans with our free, instant here:

and Advantage or Part D plans here:

Till then...

Considerations on Insuring till Medicare Starts

Here are some key concerns to look at till Medicare starts:

- Tax Credit eligibility based on Income

- Health care needs

- Doctor and facility preferences

Each of these has a role to play in our decision.

We'll explain further.

Tax Credit With Covered Ca till Medicare starts

Here's the deal.

Losing group coverage due to retirement is a qualified event that allows you to enroll in Covered California.

There can be really big tax credits in Covered Ca based on income.

It's much easier for people in their 60's to qualify for tax credits even at higher incomes so estimate your AGI for this year on the 1040 tax form (next year's tax filing) and definitely run your quote here:

.jpg)

You may be eligible for big tax credits!

If this is the case, Covered Ca will likely be the best option for you.

You can jump to the Covered Ca enrollment right here.

Especially if you're in your 60's (waiting for Medicare to start).

Here's the secret for pre-Medicare seniors with the tax credit.

Covered Ca's Secret Weapon for Individuals in their 60's

It's the perfect storm.

First, after helping 1000's of people navigate the process, one trend stands out...

The older you are, the more tax credit you can be eligible for (all other things being equal).

Give us a 25 year old with $25K income and a 63 year old with $25K and it's not unlikely to see the 63 year old get a ridiculously low rate.

Despite the fact that the underlying plan might be 2-3 times higher!

It's the tax credit.

The tax credit is tied to cost and guess what the main driver of health insurance cost is....

Age!

You can quickly see what your tax credit might be here:

- Make sure to enter your full household (even if everyone is not enrolling).

- This includes everyone that files together on a 1040 tax form even if not enrolling.

Also, use this year's best estimate for income (AGI on the 1040 tax form).

It's the fax filing you'll do next April.

One note..untaxed Social Security will need to be added to this number for the tax credit calculation.

This bring us to the next great advantage people in their 60's have with Covered Ca.

Income Advantage for Covered Ca

This period of time is traditionally when people's incomes are lower than usual.

Most have retired after all! Past years don't matter! Even last year. THIS year (next year's filing) is what we're trying to estimate now.

This lower income amount is a huge advantage to qualifying for tax credits.

Again...make sure to add standard Social Security back in!

Covered Ca plan benefits till Medicare

The tax credit is one piece of this equation...and it's a big one.

It generally makes the decision of what to do.

The other is health status.

The Covered Ca plans and Cobra will offer more comprehensive coverage than health sharing or other options.

In general, both plans:

- Cover pre-existing conditions

- Offer comprehensive benefits including preventative, rx, office, and more

- Have no annual or lifetime cap

- Can be renewed month to month for a longer period of time (Cobra will eventually exhaust)

Short term doesn't offer these protections.

That's a major difference.

If we can qualify for a tax credit, Covered Ca's probably a slam dunk.

If we don't qualify for a tax credit but have extensive health care needs and/or need coverage for a longer period of time...

Covered Ca or Cobra probably make more sense.

If we don't qualify for a tax credit, are in good health, and need the coverage for a relatively short period of time....health sharing plans might work till Medicare starts.

It's a little confusing.

No problem!

Our assistance with all three is 100% free to you and we're happy to help.

You can set up a time to chat here: https://calendly.com/dennis-jnw or email us at help@calhealth.net

There's one more very important concern....Doctors!

Doctor networks until Medicare Begins

Here's the deal...

The doctor networks with individual/family plans (such as Covered Ca) have shrunk by about 1/3rd since 2014.

It's probably the biggest issue we face (aside from cost).

You can check our doctors through the "Doctor Search" link under each plan when you run your on-exchange quote here:

If you don't see your doctor, call their office and ask them what "Covered California plans do you participate with?".

It's common to see a doctor not show up in the provider search online but find out they are actually in-network.

If your doctors do not participate and you absolutely must stay with them, Cobra might be the best option (if you can afford it).

Cobra generally has the broader networks that we miss so much.

Cobra is basically continuation of the employer health plan. You can use Cobra to keep your doctors till Medicare starts.

Of course, you have to compare this against the cost difference.

Cobra coverage can be really really expensive.

It also has a cap on the amount of time you use it for...usually 18 months.

Some people will have an 18 month Cal-cobra extension option. You can check with your prior carrier or HR department to see if this is available to you.

So, those are the big three concerns.

Let's try to re-frame it according to the three options till Medicare arrives.

Covered California till Medicare

Main attributes of this option:

- May have tax credit (could be very big); Run quote here.

- Covers pre-existing conditions

- Can renew month to month until Medicare starts

- More comprehensive coverage

- Doctor networks are smaller than Cobra

Cobra until Medicare Starts

Main attributes

- Has full employer doctor networks

- More comprehensive coverage

- Generally very expensive

Short term health between Retirement and Medicare

UPDATE: California banned all short term health insurance plans eff 9/1/2018.

In California we now only have health sharing plans that can start midnight following enrollment.

If you're eligible for a tax credit, health sharing

will not make sense.

You can quote health sharing plans here.

Information below is for States that still have short term health carrier options.

Main Short Term Attributes:

- Can be much less expensive if not eligible for tax credit

- Does not cover pre-existing conditions

- More catastrophic coverage

- Month to month in 3 month blocks; must qualify/re-apply after 3 months

Health insurance options between Retirement and Medicare Review

Lots of moving pieces.

Here's how to find the best health insurance between retirement and Medicare:

- Run quote HERE to see if you get on-exchange tax credit

- Make sure your doctors are in Covered Ca network

- Run health sharing quote here if you don't qualify for tax credit

- Go with Cobra if required doctors only participate in group network

That's how we determine which insurance is the best approach after Retirement.

Medicare's coming!

Supplements and Advantage plans will be guaranteed issue.

As licensed California agents, there's zero cost for our assistance with Medicare supplements, Advantage plans, and Part D. Learn all about them here:

Best Medicare Supplement value - Why the G plan is hard to beat

The Trade-off Between Advantage Plans and Medigap

How to pick the best Medicare Plan

Insider's Guide to Advantage Plans

Of course, we're happy to help you with any questions.

Call us at 800-320-6269 or email us.

Our assistance is 100% free to you as Certified Covered Ca and Licensed California health agents.

Again, there is absolutely no cost to you for our services.