California Medicare Options - What is the total cost for Medigare coverage

California Medicare Options - What is the total cost for Medigare coverageWhat's My Total Cost for California Medicare Coverage?

Now we're finally talking.

How much is everything going to cost me out-the-door for Medicare and the various add-on plans (supplements, Advantage, or Part D).

See...the flyers that are hitting the mailbox like the Harry Potter owl scene are only telling half (at best) of the story.

We want the good, the bad, and the ugly. With a little less ugly if possible.

We're going to break down what you can expect in terms of the total cost with Medicare along the most popular avenues.

More importantly, we're going to look at ways to save and ways you want to avoid.

Our credentials are here:

Let's get started along these lines:

- What makes up your core Medicare monthly costs

- Advantage versus Supplement costs to fill in the gaps

- How much does Part D (RX) cost

- How to compare Medicare plan costs (both monthly and total)

- Ways to save on Medicare plan costs

- How to quote and enroll in Medicare plans

Let's get started. You'll want to pass this on to friends...we're going to shed so much light on how Medicare costs work...that you may need to wear shades.

It's California after all!

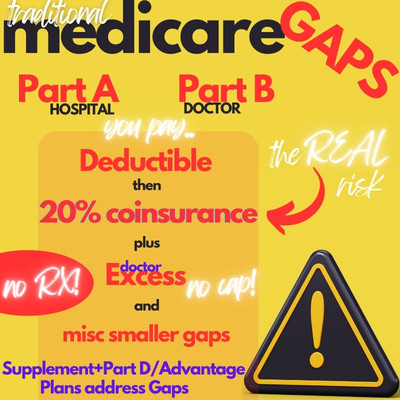

What makes up your core Medicare monthly costs

First, Uncle Sam (Medicare) has its cost!

There are two parts:

- Part A - hospital which you likely paid into all your life through payroll

- Part B - doctor; optional which requires a monthly payment

For most people, they will need to pay for Part B and the amount depends on your recent income.

The standard rate is around $202/month (changes a bit each year).

This amount can go much higher (up to over $600/month) with higher income and even lower as income drops.

You'll get your amount when you "opt-in" for Part B through Social Security.

That's cost #1 and it applies regardless of Medicare supplement OR Advantage plan.

That's where the real cost difference is. Let's go there.

Advantage versus Supplement costs to fill in the gaps

Supplements and Advantage plans fill in the basic "gaps" of Medicare:

You can think of Advantage plans as HMO options

(since most are HMO in nature) and Supplements (also called

"Medigap") as PPO options.

We have a big review on how to compare Advantage plans and Supplements but key takeaway in terms of cost:

- Medigap plans cost more monthly but generally have less out-of-pocket when

sick or hurt

- Advantage plans can be low/no cost monthly but require more cost sharing when sick/hurt

Here's the nitty gritty:

If your max out-of-pocket on the Advantage plan is over $1000, it's harder to justify it versus a G plan (the most popular supplement) unless in really good health.

This works well in the greater Los Angeles area but not so much in San Diego or the Bay Area.

We're happy to compare these two options for you or run your own free quote here.

So...what about the cost?

If we're looking only at monthly cost:

- Advantage plans will probably be zero premium; maybe expect about $800 out of pocket

annually (differs by county) on average so really, about $70/month

- Supplements (G plan) will run around $150 on average (differs by county and age) with very little out-of-pocket ($283ish for the Part B deductible with G plan).

So...now we're at (Part B monthly to Medicare + our add-on):

- Advantage: estimated around $270 ($202 part B + $70 Advantage

out-of-pocket estimate; can go much higher outside of greater Los Angeles)

- Supplement: estimate around $370 ($202 part B + $150/monthly + 20 Part B deductible monthly)

A few caveats.

- Your area and age (a big driver for Medigap) will affect the supplement

cost!

- The out-of-pocket is a rough estimate.

- Some areas have Advantage plans with max-out-of-pockets around $3000!

- Part B cost is based on income; yours may vary

- There are other supplements that are less costly but they trade off Medicare's Excess risk (learn more)

So this, this is a rough sketch! Again, we're happy to do this with

more precision for you!:

One final piece to calculate our damage!

How much does Part D (RX) cost

Traditional Medicare nor the new supplements cover medication.

For this, we need a separate Part D plan with a private carrier.

Any Advantage plan worth having will include Part D! We don't recommend Advantage plans that exclude Part D unless you get meds through some other means.

Part D plans can run from around $10-15 up to $50/month on average.

Most people find a high-rated plan at around $20 so let's go with that.

Now, we have the grand total monthly (based on an estimated out-of-pocket of $800):

- Advantage plan cost: Advantage: estimated around $270 ($202 part

B + $70 Advantage out-of-pocket)

- Supplement: estimate around $400 ($202 part B + $150/monthly + $20 Part B deductible + $20 Part D)

Keep in mind that there can be out-of-pocket for medication costs which aren't included. This is just a rough estimate of our monthly.

Assume maybe another $100 (5 meds at $20/month) added to either cost depending on your medication needs.

So...we're looking at about $3K annually with the Advantage plan and around $5K annually for Medigap/Part D coverage.

We look at why we need some protection versus just Medicare alone (more on that below with spiraling healthcare costs).

There's no cap to the 20% coinsurance with Medicare.

We're seeing bills in the millions lately for hospitals which unfortunately, is way too common now.

You don't want to be responsible for $100K of a $500K bill!

There is one big consideration if you're eligible for Medi-Cal.

The effect of Medi-cal on cost

It's estimated that roughly 20% of Californians are "dual eligible".

This means they're eligible for Medicare and Medi-cal.

This can bring down the costs for Part B (via income) and even out-of-pocket expenses with Advantage plans.

Check with the local county to see what you're eligible for and quote accordingly! Let us know at help@calhealth.net and we can run the plans that take advantage of the eligibility (called "medi medi"). See medi-medi plans or Los Angeles medi-medi to learn more.

Chronic illnesses also have specific Advantage plans that may bring down the cost.

So...how do we compare the plans taking into account our new cost information?

How to compare Medicare plan costs (both monthly and total)

First, find out what your Part B cost (based on prior income) from Social Security

Keep in mind this number may go down in later years if your income is dropping (retirement, etc)

Advantage plans are low/no premium which seems so wonderful in the flyers.

We show why this works when the max-out-of-pocket (your total exposure) is under $1000 versus supplements at our How to Pick best Medicare plan or the Trade-off with Advantage plans.

If the max is over $2000, that's like you're adding the G plan monthly premium...just paying it on the backend if you have bigger medical bills

This is the wrong time to take the bet that you won't have healthcare costs:

That's the age piece but healthcare costs are not your friend in this gamble either:

So...if you have Advantage plans with maxs under $1000, it's viable. Otherwise,

we have to consider our true out-of-pocket (monthly AND cost sharing when sick

or hurt).

Don't get tricked! We're happy to run this comparison for you and there's no cost for our assistance for either Advantage OR Medigap plans.

Alright...anything we can do to bring down these costs?

Ways to save on Medicare plan costs

Advantage plans can bring down the costs if you're in an area with low max-out-of-pockets and you're in pretty good health or have Medi-Cal.

Keep in mind that you'll trade the size of provider networks and how care is managed.

Within the supplement side, you can look at the high deductible G plan or the N plan to bring costs down.

Worst case, there's the simple A plan to cover the 20% coinsurance.

We have a great review comparing what medigap plans cover and how to value them.

Personally, we prefer the G plan or G plan with high deductible since they cover Medicare Excess (learn why) but we can go with the N plan if we understand we'll need to stay in the Medicare network (maybe lose around 2-3% of the doctors or have to pay more if we see them).

With these options, we can bring down the Medigap cost by quite a bit.

By how much you say??

How to quote and enroll in Medicare plans

Medicare plan costs are based on area and age.

Run your personalized quote here:

The Advantage plans to have a separate quote based on your doctor and RX info so

they can be personalized.

We're happy to analyze your options just like we did above to find the "sweet spots" for Advantage versus Supplements/Part D.

Advantage may be great in your area or they may be terrible (high max out of pocket).

We'll let you know and quote the costs for the following as a benchmark:

- Highest rated Advantage plans with low/no premium and lowest out-of-pocket

max

- Best priced G plan

- Best priced G plan with high deductible

- Best priced N plan

- Best Priced A plan

- Best Priced/Rated Part D (if you're getting a supplement)

Just run your quote above and we'll send this all to you. There's no cost for our assistance and check out our Google reviews!

We work with the strongest California Advantage and Medigap carriers that work with private hospitals/doctors.

Now...how many lattes pay for one supplement?